One of the most complex issues in project finance modeling is multiple debt sizing and sculpting. Let’s work through a case study.

Assumptions:

- Two senior debt tranches with different terms

- Bank 1, the Development Bank, has a 12-year tenor and 5% interest rate (Dev_Rate)

- The Development Bank has communicated that it wants to fund 49% of total senior debt (no crowding out)

- Bank 2, the Commercial Bank, has an 8-year tenor and 10% interest rate (Comm_Rate)

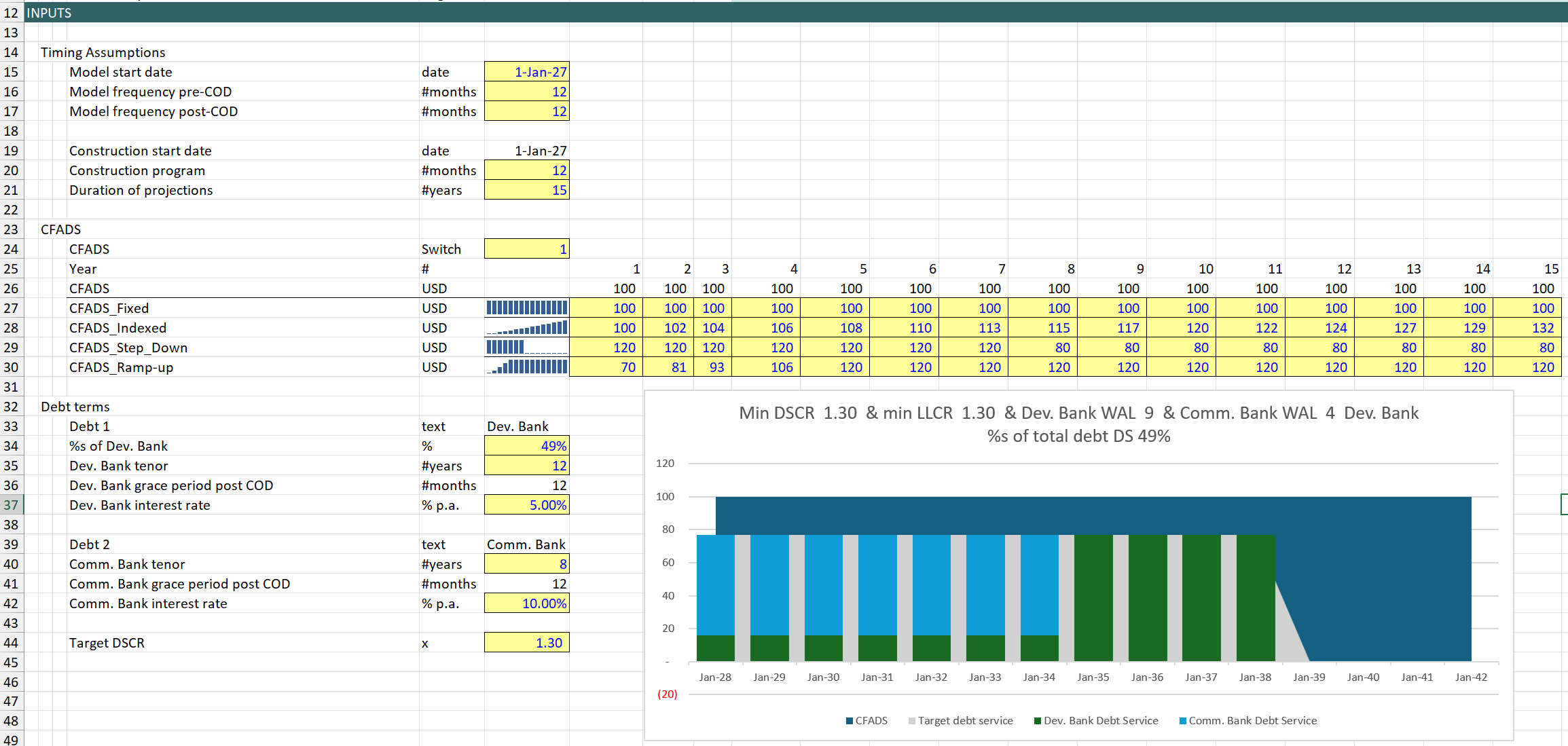

- The lender consortium has agreed on a base case DSCR of 1.3x (a 23% cash buffer for downside risk)

- You have already built a model and calculated the cash flow available for debt service (CFADS)

The questions to answer are:

- What is the total maximum debt this cash flow can sustain?

- What is the Development Bank’s share of total debt which then gives us the Commercial Bank’s share by difference.

- How are the Development Bank and Commercial Bank principal repayments sculpted and repaid?

Calculations:

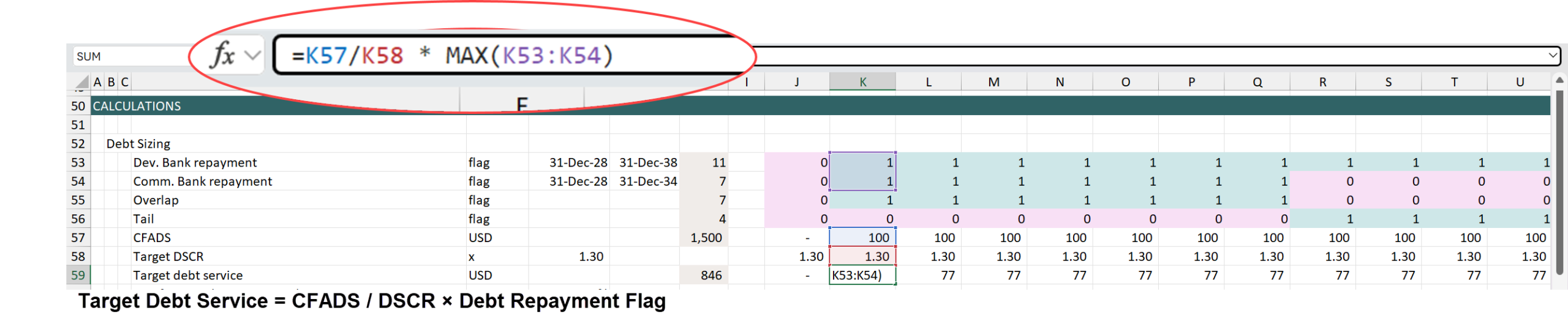

Step 1: We start with CFADS and derive the Target Debt Service.

Target Debt Service = CFADS / DSCR × Debt Repayment Flag

Step 2: Target Debt Service can be split into two components:

Target Debt Service = Target Debt Service during Overlap + Target Debt Service during Tail

When sizing and sculpting the Development tranche, we allocate a percentage share of Target Debt Service during the overlap period to the Development Bank; during the tail period, 100% of target debt service is available to the Development Bank. The key question is: what is the percentage split of debt service between the two banks during the overlap?

After reviewing hundreds of project finance models throughout my career, the most common approach I’ve seen is a goal seek to find the percentage split. But before going down that route, let’s look at the math.

Step 3: From present value to debt sizing:

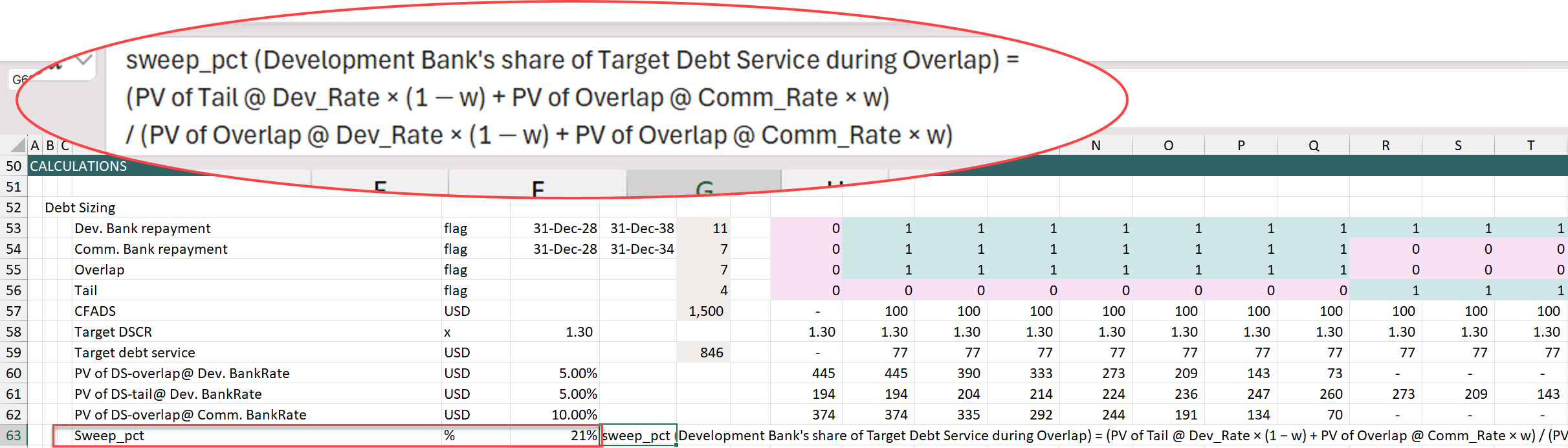

Let’s call the Development Bank’s share of target debt service during the overlap period sweep_pct.

Development Bank Debt Service = Target Debt Service during Overlap × sweep_pct + Target Debt Service during Tail

Commercial Bank Debt Service = Target Debt Service during Overlap × (1 − sweep_pct)

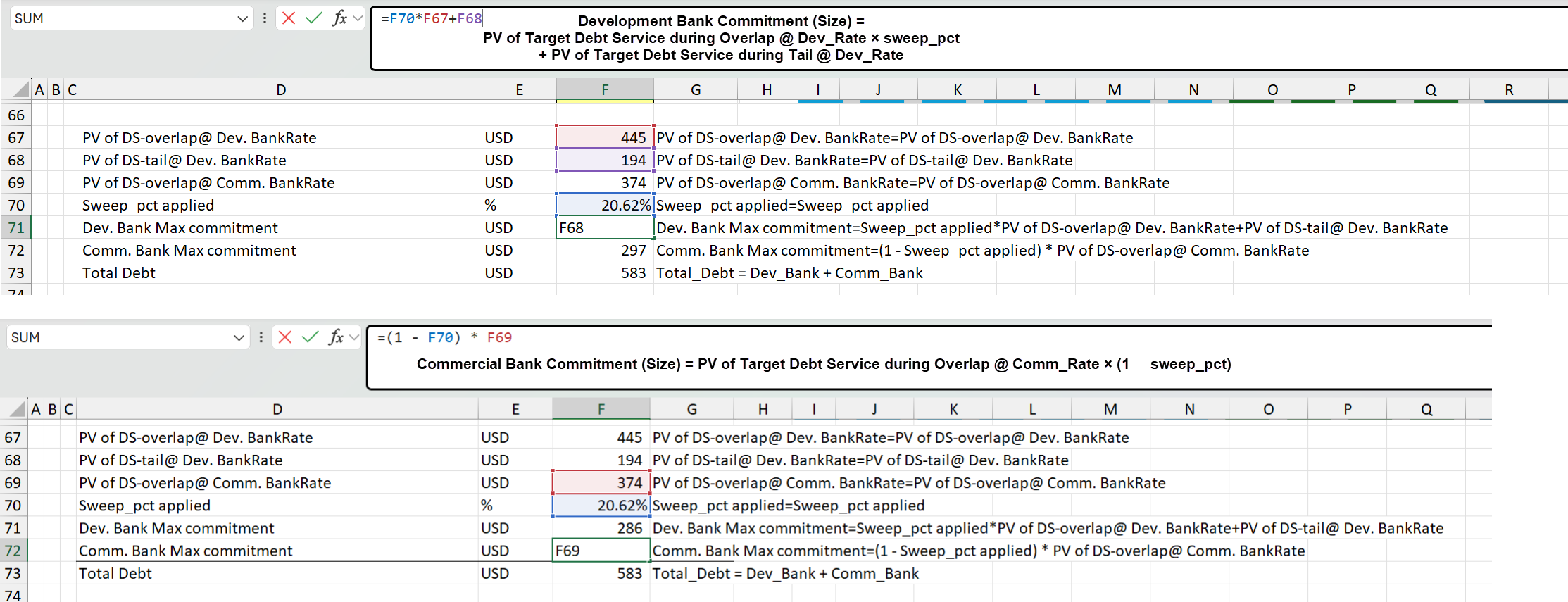

Development Bank Commitment (Size) = PV of Target Debt Service during Overlap @ Dev_Rate × sweep_pct + PV of Target Debt Service during Tail @ Dev_Rate

Commercial Bank Commitment (Size) = PV of Target Debt Service during Overlap @ Comm_Rate × (1 − sweep_pct)

So what is the sweep rate?

Let’s define variables for clarity:

- Dev_Bank = Development Bank Commitment (Size)

- Comm_Bank = Commercial Bank Commitment (Size)

- A = PV of Target Debt Service during Overlap @ Dev_Rate

- B = PV of Target Debt Service during Tail @ Dev_Rate

- C = PV of Target Debt Service during Overlap @ Comm_Rate

- w = Development Bank’s share of total debt (49%)

So:

Dev_Bank = A × Sweep_pct + B

Comm_Bank = C × (1 − Sweep_pct)

We have one constraint: the Development Bank’s share must not exceed 49%. We can use this to derive the required Sweep_pct.

w = Dev_Bank / (Dev_Bank + Comm_Bank)

w = (A × Sweep_pct + B) / (A × Sweep_pct + B + C × (1 − Sweep_pct))

Cross-multiplying:

A × Sweep_pct + B = w × A × Sweep_pct + w × B + w × C − w × C × Sweep_pct

Moving all Sweep_pct terms to the left and constants to the right:

A × Sweep_pct − w × A × Sweep_pct + w × C × Sweep_pct = w × B + w × C − B

Factoring out Sweep_pct on the left:

Sweep_pct × (A × (1 − w) + C × w) = B × (1 − w) + C × w

Therefore:

Sweep_pct = (B × (1 − w) + C × w) / (A × (1 − w) + C × w)

sweep_pct (Development Bank’s share of Target Debt Service during Overlap) = (PV of Tail @ Dev_Rate × (1 − w) + PV of Overlap @ Comm_Rate × w) / (PV of Overlap @ Dev_Rate × (1 − w) + PV of Overlap @ Comm_Rate × w)

Step 4: Debt Sizing and Sculpting

Now we have everything to calculate the debt sizing and sculpting of both tranches:

Development Bank Commitment (Size) = PV of Target Debt Service during Overlap @ Dev_Rate × sweep_pct + PV of Target Debt Service during Tail @ Dev_Rate

Commercial Bank Commitment (Size) = PV of Target Debt Service during Overlap @ Comm_Rate × (1 − sweep_pct)

Development Bank Debt Service = Target Debt Service during Overlap × sweep_pct + Target Debt Service during Tail

Commercial Bank Debt Service = Target Debt Service during Overlap × (1 − sweep_pct)

What I love about this approach is that it makes the logic transparent and forces us to think about the problem from a different angle. That said, my concern is how it holds up for the next step: more than two tranches. The math gets considerably more complex there. My preferred approach is Professor Edward Bodmer’s method, the LLCR approach, which I have covered in other posts.

What I love about this approach is that it makes the logic transparent and forces us to think about the problem from a different angle. That said, my concern is how it holds up for the next step: more than two tranches. The math gets considerably more complex there. My preferred approach is Professor Edward Bodmer’s method, the LLCR approach, which I have covered in other posts.

You can reach me at hedieh.kianyfard@gmail.com, or contact Professor Edward Bodmer at www.edbodmer.com

We are happy to talk further.

And if this raised questions for you, especially around what happens when the 49% constraint is binding versus when it is not, drop them in the comments. I read every single one.